30 March 2026

This article was first published on LinkedIn as part of the Signals over Noise newsletter.

It's been over three years since ChatGPT launched and sent a wave of GenAI disruption around the world. We've seen the full spectrum — massive transformation in some areas like software development, and near-zero impact in others. So where does automotive sales land on that spectrum? Has the customer experience actually improved, and if so, where did it happen — and what comes next?

1. Car Advisor

Current Impact: Medium | Future potential: High

I've previously critiqued BCG's and OpenAI's paper on GenAI as a car advisor tool, and I remain cautious about OEMs trying to control what LLMs output. That said, the evidence is clear: customers are already using generic LLMs (like ChatGPT) in their purchase journey — particularly for information seeking — whether the industry is ready for it or not.

Online community discussions indicate that the use cases tend to cluster around three types of questions:

- Comparative brand or model analysis (e.g., asking ChatGPT which brand is most reliable, or asking Gemini to identify the winner within a specific segment)

- Practical calculations and planning (e.g., asking Claude to compute A/C battery drain, or using ChatGPT to map out a charging route from Bangkok to Chiang Mai)

- General research on unfamiliar topics (e.g., asking ChatGPT to summarize why EV insurance is expensive)

The quality of what gets shared looks reasonably solid at first glance — AI-generated answers are structured, cover multiple angles, and seem to genuinely inform the discussion. But the community's reaction is telling: people treat these outputs as conversation starters, not conclusions, often explicitly asking others whether they agree with what the AI said.

One user who tried an LLM for a specific charger troubleshooting problem got nothing useful and turned to the community instead — a reminder that for niche, market-specific questions, human networks still outperform AI. And the fact that online discussion volumes haven't dropped — they've actually grown — suggests GenAI is filling some roles in the research journey, but is far from replacing the community as the only car advisor.

Implications for automotive distributors

For OEM distributors (including National Sales Companies and independent importers), the most immediate consequence is a more informed — and more demanding — buyer. Spec comparisons that once required an hour across multiple websites now take seconds. But the more interesting implication sits one layer deeper. If GenAI makes rational, spec-based comparisons effortless, the next natural question becomes harder to deflect: why does this brand cost more for a similar or lower-speced model? Customers can now check the numbers, read owner feedback, and compare alternatives much more easily. As a result, factors such as brand heritage, product design, network quality, and after-sales reputation matter more explicitly. Brands can no longer rely on customer confusion or limited visibility to protect a weak value proposition.

For OEMs with strong intangible differentiation, this could actually be an opportunity. For those whose premium pricing rests on legacy perception rather than genuine product superiority, it's a risk that will only grow as GenAI literacy among car buyers increases.

2. Online Lead Conversion

Current Impact: Low | Future potential: Medium, but low short-term

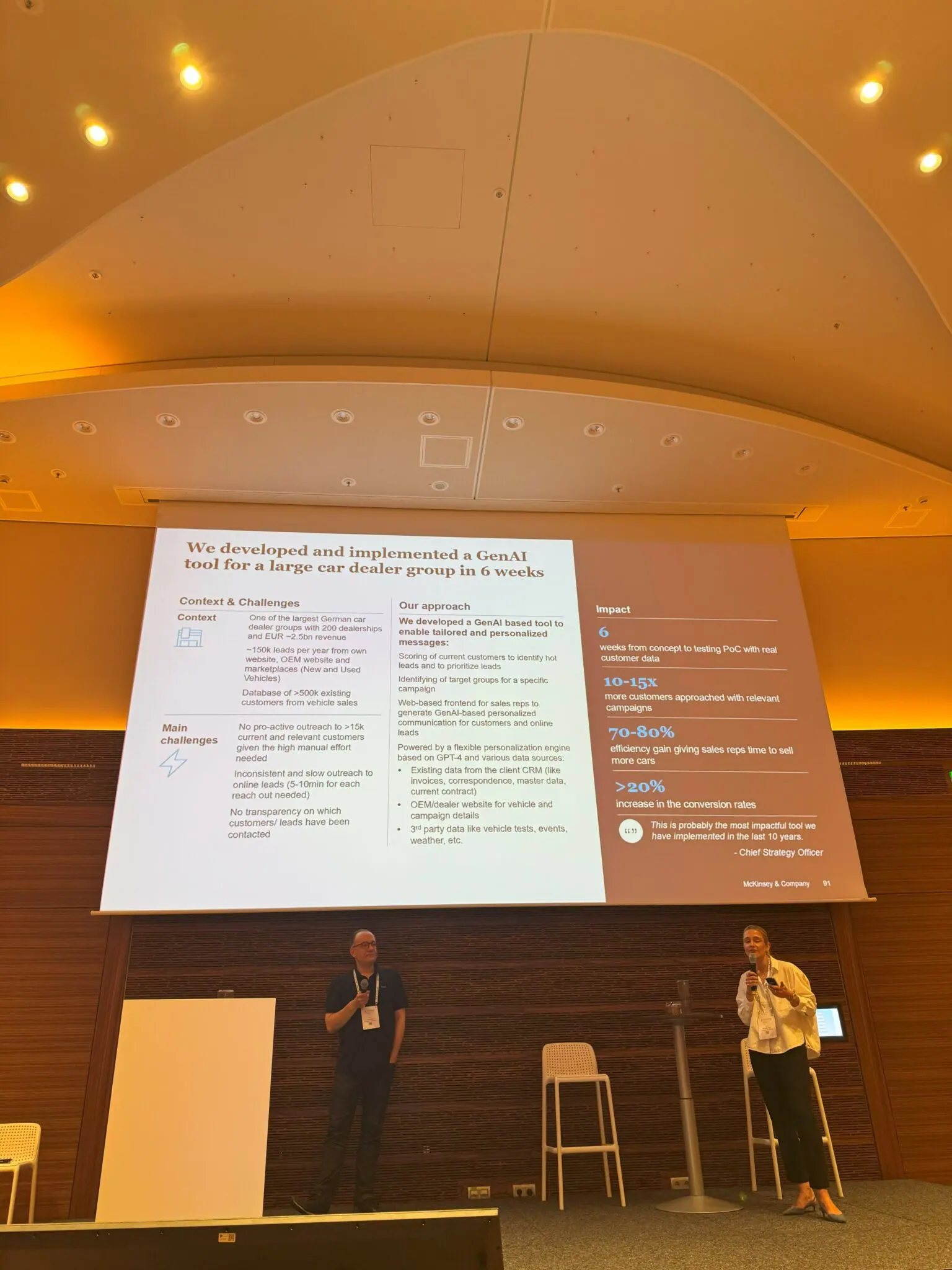

The area where GenAI deployment in automotive sales seems to have delivered some commercial results is lead management. McKinsey's work with a large German dealer group offers a useful concrete example: a GenAI tool built in six weeks that scored existing customers to identify hot leads, generated personalized outreach messages, and reduced response time to online inquiries from around 10 minutes to 2 minutes. The reported outcomes were significant — a 70-80% efficiency gain for sales reps and a conversion rate increase of over 20% (translating to an estimated 15-25 additional vehicle sales per sales rep per year). The Chief Strategy Officer called it the most impactful tool implemented in the last ten years.

Source: Autovista24

These results are plausible and worth taking seriously. But the preconditions in that case were likely strong, as even the pre-GenAI response time — 10 minutes — was already good by many standards. In Southeast Asia, that time is often counted in days and sometimes the response never comes. It is therefore reasonable to assume that other key enablers such as rich CRM, consistent data, and organizational willingness to act on GenAI outputs — which are far from universal — were also likely there and making the tool implementation easier.

In Southeast Asia specifically, most distributors and dealer groups are nowhere near that starting point, which is why similar impact remains difficult to achieve. Why is that the case though?

The implicit assumption underneath all of this seems to be that a serious buyer will find their way to the dealer regardless, mostly driven by product and price attractiveness rather than the sales experience itself. If they really want the car, they'll call. If one dealer does not pick up or does not have the car available, then the customer will find another dealer who does. So will there be any change then? The honest answer is probably not anytime soon.

Implications for automotive distributors

Two scenarios could realistically force the shift. The first is distributors making a strategic decision to keep the dealer network as streamlined as possible — accepting that fewer, better-run dealerships could maintain volumes while actually creating pressure to optimize each customer interaction. This runs directly against the current rule of thumb, where a wider network means more wholesale touchpoints and distributed risk. Don't hold your breath.

The second is a player taking the risk of genuinely raising the bar on customer experience — investing in the data infrastructure, the follow-up discipline, and potentially the AI tooling — and being rewarded for it visibly enough in sales and customer satisfaction that others are forced to take notice. This too requires someone to absorb short-term cost and organizational pain for long-term gain, which may or may not come to fruition.

Neither scenario seems imminent. Hence, the customer will need to find his way, or pick a different brand instead.

3. After-Sales Customer Experience

Current Impact: Low | Future potential: Medium, but low short-term

After-sales customer service is, on paper, one of the most logical places for GenAI adoption in automotive. The reasons are straightforward: most service queries are high-volume and repetitive — exactly what GenAI handles well. Unlike sales interactions, service queries typically follow defined resolution paths grounded in policies and FAQs, which limits the downside when GenAI gets something slightly wrong and makes human handoff easier to design. GenAI also removes constraints that humans can't escape: working hours, memory of past service records, and the operational cost of staffing customer support across multiple channels.

That said, none of this means GenAI is automatically the right tool. For many customers, a well-functioning app that does a couple of important things reliably — e.g., book a service appointment, reschedule it, confirm it — can be sufficient, whether the app is GenAI-powered or not.

The more pressing problem in Southeast Asia is that the basics aren't working on a wider scale yet. Several brands in Thailand do offer mobile apps or online service scheduling. But fragmented IT systems, limited integration between OEM and dealer platforms, and poorly designed workflows mean that many of these tools are not fully automatic in practice. Bookings still don't link well with dealers' backend systems and require a phone or LINE confirmation from the dealer — which may or may not arrive — leaving the customer in limbo and pushing them back to calling the dealer directly. The online tool may exist. The experience it was supposed to create doesn't.

Adding a GenAI layer on top of these systems will not fix them. It will make the failure more sophisticated.

Implications for automotive distributors

Two mindset shifts are required, and neither is primarily about technology.

The first is treating after-sales digital experience as something with a measurable return rather than a sunk cost. This matters more than it once did. In an era where spec comparisons take seconds and product differentiation is increasingly difficult to sustain, after-sales reputation travels further than most OEMs account for. According to Auteneo data, across all aspects of vehicle ownership experience, after-sales has consistently recorded the lowest sentiment score — meaning it is the dimension most actively damaging brand perception among existing owners.

The second shift is from a "build and forget" mentality to "build, monitor, improve." Customers are disappointed when an expected digital tool doesn't exist. They are arguably more disappointed when the tool exists but fails to deliver — because the brand has now created an expectation it isn't meeting. A customer who never expected to book online is not let down when they have to call. A customer who downloaded the app, tried to use it, and still had to call is.

Conclusion

Three years after ChatGPT reshaped expectations across many sectors, the automotive customer journey in Southeast Asia remains largely unchanged. GenAI is changing how buyers research cars, but the industry's response — in lead management, in after-sales, in basic digital infrastructure — has not kept pace. Sometimes, new technologies are less a transformation story and more a waiting room.